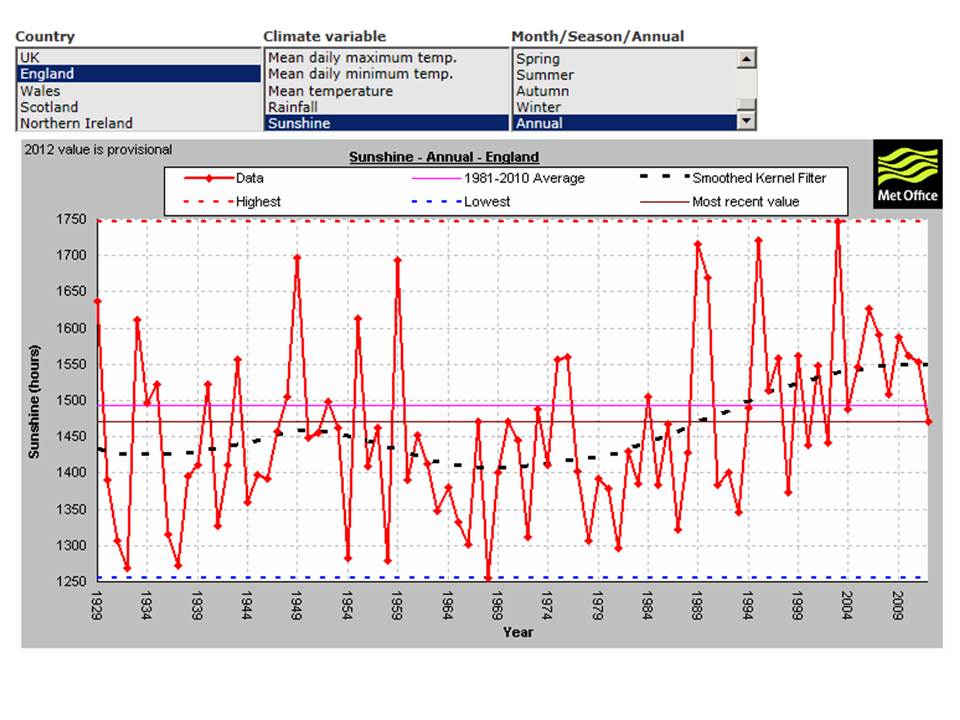

This data shows that 2012 was just slightly worse than long-term average for total hours of sunshine, so our domestic PV over-performance (see previous post) was not due to high numbers of hours of sunshine.

| One Planet Living for humanity, forever |

|

|

This data shows that 2012 was just slightly worse than long-term average for total hours of sunshine, so our domestic PV over-performance (see previous post) was not due to high numbers of hours of sunshine.

0 Comments

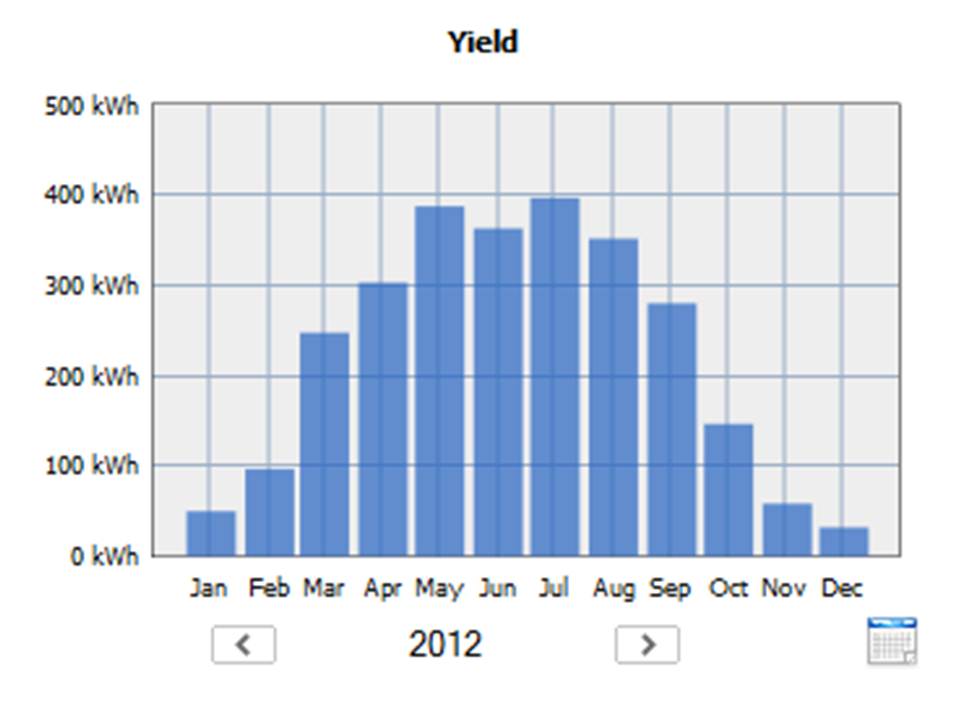

This is a 3.68 kWp domestic array, in two strings, one facing East and the other West. Total yield in the year was about 2,700 KW hours. The installer's annual generation estimate was just under 2,500 at the time of purchase. I'm not sure whether the actual over-performance is because of prudence in the installer's estimate or a better-than-average amount of sunshine last year. Anyway, I'm delighted with the performance so far.

Phil Wynn Owen from DECC (seen in the picture on the left) outlined some key challenges in keeping climate change to under 2 degrees. We need to do better in the UK to move to lower carbon energy, especially beyond 2022 at a time when a lot of existing energy generating capacity will have been decommissioned. Developments that will help are carbon budgets, the Green Investment Bank, smart meters, RHI, EMR, £110billion of infrastructure investment.

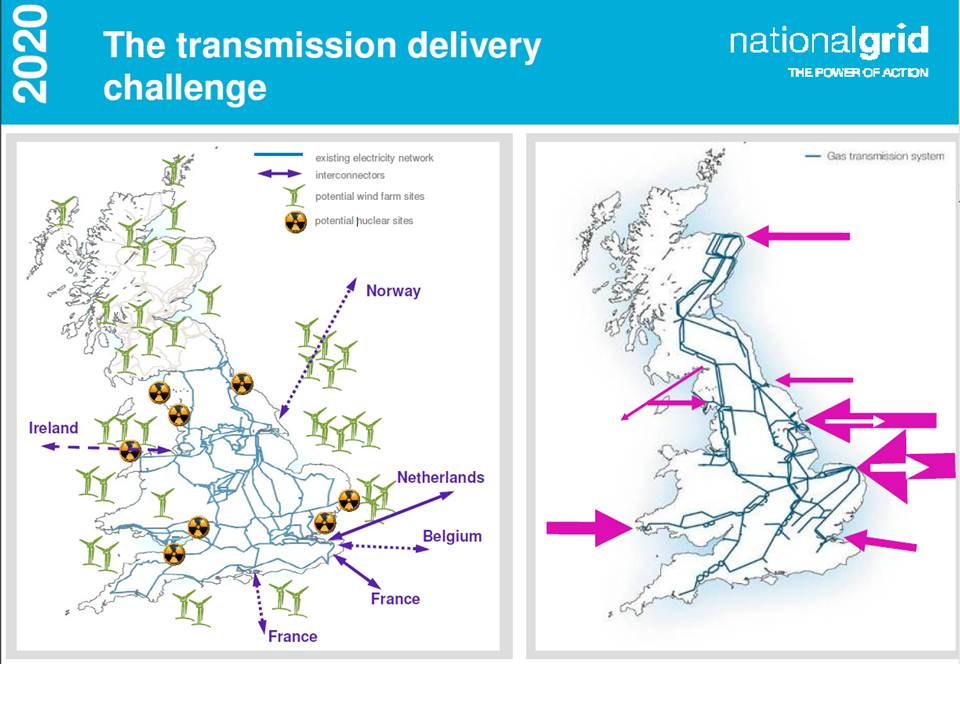

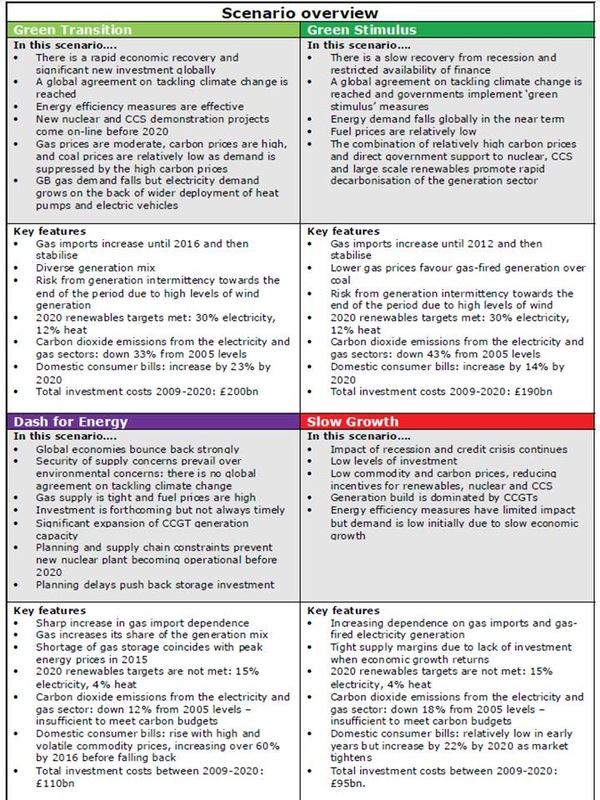

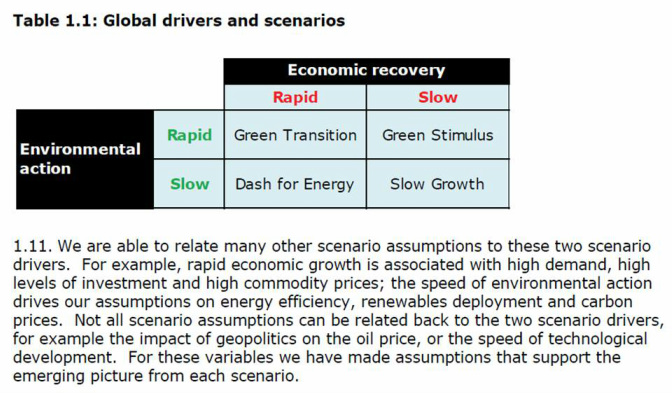

The next opportunity to facilitate international co-operation will be the COP18 meeting in Doha (Qatar) in Nov/Dec 2012. Here's a picture from a National Grid document about their own energy future scenario modelling. It illustrates why planning investment for the UK National Grid is such a complex problem, and increasingly so as the number and variety of energy generation, storage and usage nodes and volumes alters (and direction of energy flow sometimes switches).  Here's a fuller summary of the scenarios from the 2009 Ofgem Project Discovery report. It's worth giving the main caveat here, that the Discovery scenarios represent a series of diverse, but plausible and internally consistent, futures that will allow us to test current arrangements and possible future policy responses. The scenarios are not meant to represent forecasts and many other possible outcomes can be envisaged.  Here's the very summary description of the scenarios in the Ofgem Project Discovery, highlighting the main drivers they modelled in their analysis:  In their 2009 report on this project, from which the above is an excerpt, Ofgem explores a number of scenarios for the UK energy system, with the objective of informing policy decisions for delivering secure and sustainable energy supplies. They go on to say:

" Delivering secure and sustainable energy supplies means in broad terms that:

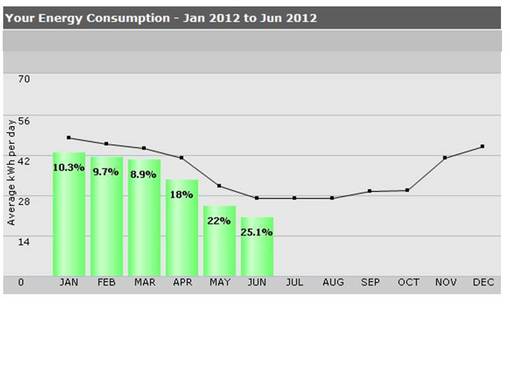

There are a couple of factors that seem to be omitted (unless they're buried in the details and I haven't spotted them yet) - the effects of Distributed Generation and Storage on the demands on, and nature of, the National Grid for electricity and gas transmission and distribution. This grid has largely, to date, been built around the existence of a relatively small number of very large power (generation) stations. With many low carbon technologies presenting opportunities to have a very large number of much smaller generating plants, with these being very widely distributed, and with the prospect of future storage solutions reducing the need to transfer as much energy via the grid, this could significantly alter how people envisage the future configuration and design of the transmission grid.  PV panels on the roof, as well as generating FIT payments, are enabling us to make significant savings on our electricity usage from the grid compared with last year, as shown by these latest figures. The percentages show the size of the reduction

“Green Growth” is a bit of an oxymoron, in the context of limits to growth, unless the “green growth” is associated with “non-green shrinkage” in some way. If it involves substitution, then I’m inclined to support it when it has the right kind of impacts on supply and usage chains. For example, for new businesses to be truly worthy of the tag

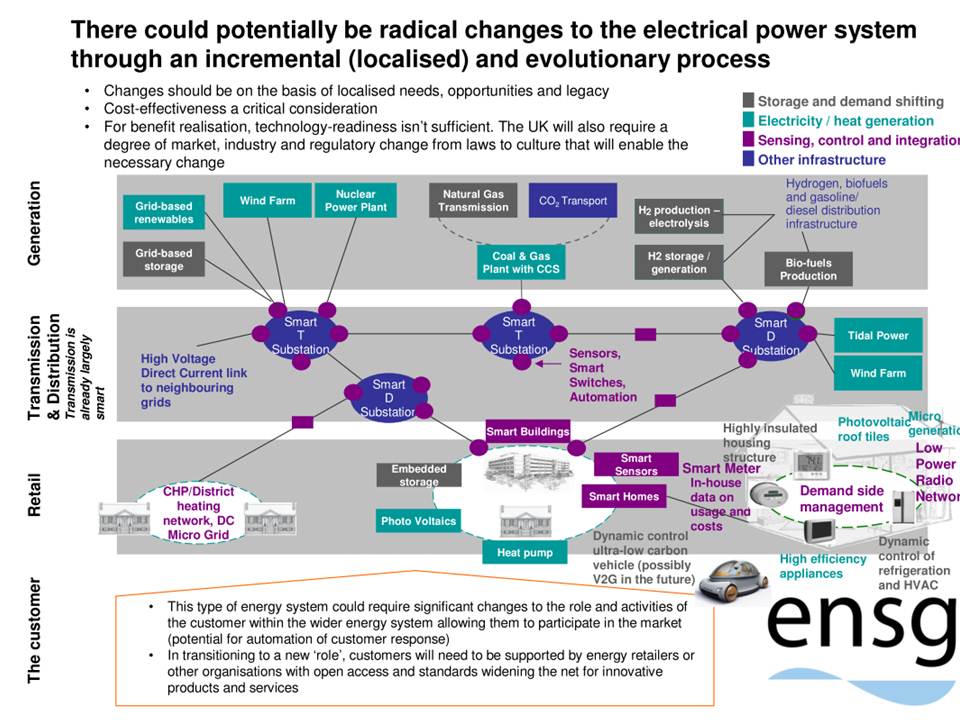

‘green’ they must be providing alternative products/services/choices which substitute for existing products/services/choices and which have more sustainable total lifecycle chains than those existing products/services/choices (taking into account both upstream of the point of supply/choice and also downstream) and sufficiently so to take us closer to long-term sustainable equilibrium positions. They should take into account all the impacts of that substitution (positive and negative) in arriving at this ‘calculation’. A case in point is the current mini-goldrush for solar PV in the UK domestic sector – it’s good that this results in some non-fossil-fuel energy generation substituting for grid-supplied electricity (at its current mix of fossil-fuel and non-fossil-fuel energy). However, there is a downside to the inherent inefficiencies of lack of scale for each individual installation, and an ecological footprint resulting from the manufacture of the panels (mostly in China, using a high proportion of coal-fired energy) and extended supply chains for transportation of the PV panels over large distances to get to the installation site. I haven’t seen the total life-cycle impact analysis for a typical installation, but I certainly hope it is a positive ‘eco-NPV’ (if I could call it that) – and a lot more eco-friendly than small domestic wind turbines which, by reputation, have a very poor total lifecycle eco-calculation. Anyway, such an eco-NPV, if calculated, could provide the basis for saying that the ‘green growth’ in the solar PV manufacture and supply chain was a good thing, because of having a positive net eco-effect after considering the alternative national grid energy substituted. Of course, these benefits aren’t as great on a short-term marginal basis as they are in the longer-term, when for example it might be possible to avoid building an oil or gas power station (or decommission an existing one sooner than previously planned) because of the number of PV installations up and down the country at that time - that’s the point at which the benefits are most visible. However, at that point there is a big negative if the real substitution going on is the substitution of a new coal-fired power station in China for the oil or gas power station not built (or decommissioned) in the UK! Although it's good to see DECC providing incentives to increase uptake of green energy generation, more needs to be done to tackle the deep-rooted deficiencies, barriers and inertia in the existing financial and economic paradigm. The following is from Paper 1 on the Green Economy from RIO+20 in June 2012: "Attempts merely to overlay ‘green growth’ onto the finance driven model of economic globalisation, will be like setting freshly spawned fish to swim against a flood tide. The proposers of the Green New Deal dwelt on finance so much, precisely because it is the rock upon which sustainability repeatedly flounders." More information about Green New Deal at: (link). The following is a particularly good paragraph, from the same paper, setting out the challenge to the existing growth paradigm: "Stop assuming that all GDP growth is good, and a panacea for all other objectives. Firstly it isn’t, there is jobless growth, growth with rising inequality and growth that masks qualitative decline within an economy. Secondly, continual GDP growth is incompatible with acknowledging inescapable planetary boundaries. Work by nef [New Economics Foundation], the Tyndall Centre for Climate Research and others have demonstrated this. No one has successfully demonstrated the opposite. Time and again, growth swamps gains from efficiency and technological innovations. Instead, start from the explicit premise that the economy must operate within given environmental parameters. Also, begin with a vision of what the economy is for, namely, to deliver the chance of relatively long and happy lives for everyone on the foundations of social justice for all. The current growth paradigm, even with heroic levels of ‘green innovation,’ cannot, without reduced overall consumption, on its own keep within environmental limits and deliver poverty alleviation and greater equality. This is not to say that necessary economic activity in some sectors and in many parts of the world will not contribute to GDP and localised growth. During transition to a low carbon, lower consumption economy, sectors that are key will expand. " This event , organised by the Smart Energy Special Interest Group (SESIG) of the Technology Strategy Board, was illuminating, dealing with various aspects of the DECC-led £11billion drive to install smart meters in all UK households by 2017. As I understand it, smart meters have two main uses - by the householder in understanding and managing their energy usage in the home, and by 'the utilities' and regulators in managing the grid, the demands on the grid and the energy generation inputs to the grid from renewables and from more traditional sources. Although the funding model is not yet clear, it is clear that a lot of work (including work on a number of pilot projects under the auspices of the Technology Strategy Board) is happening to enhance understanding of many of the detailed technical, supply chain and consumer-engagement aspects, to feed into the design of the rollout programme. It is expected this will have some complementarity with the Green Deal initiative from Autumn 2012. Conference materials are expected to be available soon, and the SESIG is also promoting a new online resource - an Energy Base - an open, public-domain, wiki-style repository of relevant information for all to access, use and contribute to. Below is one of the core overview diagrams referenced on the day - from a strategy paper issued by Electricity Networks Strategy Group (ENSG) in about 2009 but still very relevant today.  |

About the BloggerI'm David Calver - an Accountant with a passion for sustainability. Categories

All

Archives

February 2016

|

RSS Feed

RSS Feed